Our planning for 2026 is based on the assumption that global economic output will grow overall, albeit at a slower pace than in 2025. We continue to see risks related to the development of the general economic environment in the increasing fragmentation of the global economy and protectionist tendencies, in turbulence in the financial, energy and commodity markets, as well as in structural deficits in individual countries. Growth prospects are also weighed down by continuing geopolitical tensions and conflicts; risks stem in particular from the Russia-Ukraine conflict, the escalation in the Middle East, as well as growing uncertainties regarding the policy stance of the USA and the global increase of geoeconomic measures, which could further exacerbate geopolitical tensions. We anticipate that both the advanced economies and the group of emerging markets will exhibit on average momentum that is slower than in 2025.

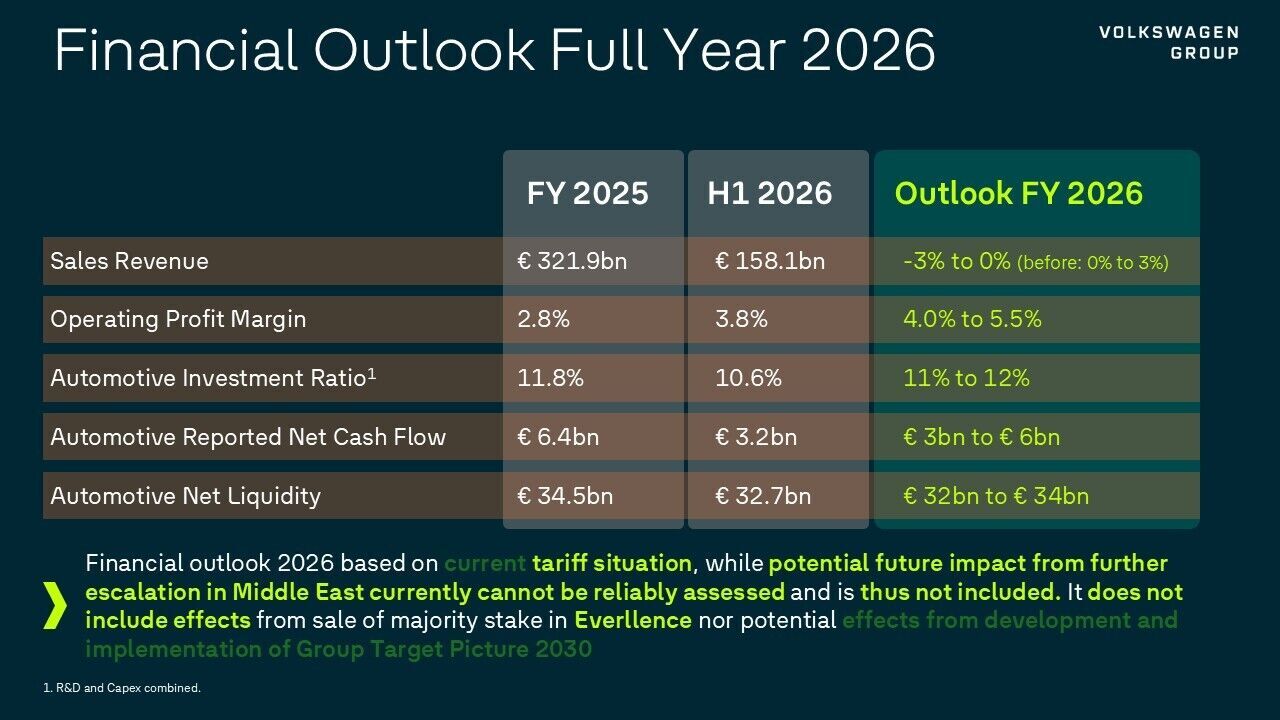

The trend in the automotive industry closely follows global economic developments. We assume that competition in the international automotive markets will continue to increase. Crisis-related disruption to the global supply chain and the resulting impact on vehicle availability may weigh on new registration volumes. Moreover, suddenly arising or intensifying geopolitical tensions and conflicts could in particular result in rising prices and declining availability of materials and energy, and necessitate a reassessment of existing resource allocations. We predict that trends in the markets for passenger cars in the individual regions will be mixed in 2026. Overall, global new vehicle sales volumes are expected to be slightly below the level of the previous year. In Western Europe, we anticipate that the volume of new passenger car registrations in 2026 will be slightly higher than the prior-year level. For the German passenger car market, we expect the volume of new registrations in 2026 to be in the range of the previous year. We anticipate a strong year-on-year increase in sales of passenger cars overall in markets in Central and Eastern Europe – subject to further developments in the Russia-Ukraine conflict. In the markets for passenger cars and light commercial vehicles (up to 6.35 tonnes) in North America overall, as well as in the USA, sales volumes in 2026 are forecast to be slightly below the previous year’s level. The number of new registrations in the South American markets in 2026 is projected to show a significant overall year-on-year increase. The passenger car markets in the Asia-Pacific region in 2026 are expected to be noticeably down on the prior-year level. Trends in the markets for light commercial vehicles in the individual regions will be mixed; on the whole, we expect the sales volume for 2026 to be in the range of the figure recorded the previous year. For 2026, we expect that new registrations for mid-sized and heavy trucks with a gross weight of more than six tonnes will be slightly above the level of the previous year in the markets that are relevant for the Volkswagen Group, with regional variations. A noticeable year-on-year decrease in demand is anticipated for 2026 in the bus markets relevant for the Volkswagen Group, but this will vary depending on the region. We assume that automotive financial services will continue to play an important role in global vehicle sales in 2026, in conjunction with the development of vehicle markets. In light of significant market volume declines in China, we expect deliveries to Volkswagen Group customers to decrease by -7.0% to -3.0% in 2026. Uncertainties relate in particular to the economic environment, international trade restrictions and geopolitical tensions, intensifying competition, volatile commodity, energy and foreign exchange markets, and changing emis sions-related requirements. We expect the sales revenue of the Volkswagen Group to develop within the range of –3.0% to 0% year-on-year in 2026. The operating return on sales for the Group is projected to be between 4.0% and 5.5%. We assume that the investment ratio in the Automotive Division will lie between 11% and 12% in 2026. We expect net cash flow for 2026 to be between €3 billion and €6 billion. Net liquidity in the Automotive Division in 2026 is expected to range between €32 billion and €34 billion. We remain committed to continuing our robust financing and liquidity policy. The forecast is based on the assumption that the current tariff situation in international trade will persist. Potential future effects of the escalation in the Middle East cannot be reliably estimated, which is why they are not included in the KPI projections. The forecast is based on the Volkswagen Group’s current structures and does not factor in possible impacts from the development and implementation of the 2030 Group Target Picture or from the disposal of the majority shareholding in Everllence.

Wolfsburg, July 24, 2026